https://www.bloomberg.co.jp/news/articles/2022-05-23/RCCBP0DWX2PW01

ECBブログはこれ↓

https://www.ecb.europa.eu/press/blog/date/2022/html/ecb.blog220523~1f44a9e916.en.html

Monetary policy normalisation in the euro area

Blog post by Christine Lagarde, President of the ECB

Frankfurt am Main, 23 May 2022

Since December last year, the ECB has been starting the journey down the path of policy normalisation.

This process began with our announcement that we would end net asset purchases under the pandemic emergency purchase programme (PEPP) in the first quarter of this year. That has now been done.

The process continued with our announcement of an expected end date for net purchases under the asset purchase programme (APP). And as the inflation outlook has evolved, we have also adjusted our communication on the likely timing of interest rate lift-off, in line with our forward guidance.

As a result, investors have been progressively updating their expectations of the ECB’s policy intentions. This has been reflected in a revision of interest rate expectations and an upward shift in real rates at the longer end of the yield curve.

A policy adjustment has thus already been working its way through the euro area economy over the past six months.

But as the expected date of interest rate lift-off draws closer, it becomes more important to clarify the path of policy normalisation that lies ahead of us – especially given the complex environment that monetary policy in the euro area is facing.

This is the purpose of my blog post today.

The changing environment facing monetary policy

Monetary policy normalisation is not a predefined concept: it depends crucially on the environment we are facing and the nature of the shocks hitting the economy. Today, our economies are reopening but we are not re-entering the world we left behind in early 2020 when the pandemic broke out.

At that time, the euro area economy had been in a prolonged period of too-low inflation. Headline inflation had averaged 1.1% since 2012 and core inflation just 1%. On the eve of the pandemic, the prices of less than 20% of the items[1] in the core inflation basket were increasing above 2%. Inflation was forecast to be just 1.6% in 2022.

The factors behind this low inflation were complex, reflecting an interaction of persistent demand weakness, structural forces and sliding inflation expectations.

In particular, the slow recovery from the great financial crisis and sovereign debt crisis led to a lingering demand gap, while structural forces – such as globalisation and digitalisation – were in parallel producing positive supply shocks, weighing on inflation and wage growth.

In this context, realised inflation drifted down and, with interest rates nearing the effective lower bound, inflation expectations followed. Measures of longer-term market-based inflation compensation had dropped to around 1.25% before the pandemic.

There was a genuine risk of too-low inflation becoming entrenched – and that is why the ECB’s policy settings were fully focused on dislodging this disinflationary environment.

The new inflation landscape

Today, the conditions facing monetary policy have changed markedly. Three shocks have combined to push inflation to record highs.

First, we have faced a series of shocks to input prices and food prices.

These include the failure of OPEC+ to meet production targets, rising natural gas and hence fertiliser prices, and now the ramifications of the war in Ukraine. All this has led to surging energy and food prices, with the relative price of energy rising far higher than the individual spikes experienced in the 1970s.[2]

Second, we have faced shocks to both the demand for and supply of industrial goods, which has shown up in record-high industrial goods inflation.

Demand has been stoked by stimulus policies in major economies and the forced switch in consumer spending from services to goods during the pandemic. Supply, on the other hand, has been constricted by the sluggish rebound of industrial production from lockdowns, transport and logistics bottlenecks, and now “zero COVID” policies in China once again.

Third, we have had the shock from economies reopening after lockdowns, which has triggered a rapid rotation of demand back to services – all while input costs have been rising and companies in the services sector, especially in tourism and hospitality, have struggled to find staff quickly enough to meet rising demand. That has led to rising services inflation.

This unprecedented combination of shocks has been reflected in broader and more prolonged inflation pressures. Core inflation jumped to 3.5% in April. And because all sectors of the economy are being affected, 75% of items[3] in the core inflation basket are now recording inflation rates above 2%.

On top of these conjunctural shocks, we are also seeing a partial reversal in some of the structural trends that had helped hold down inflation over the past decade.

The Russia-Ukraine war may well prove to be a tipping point for hyper-globalisation, causing geopolitics to become more important for the structure of global supply chains. That could lead to supply chains becoming less efficient for a while and, during the transition, create more persistent cost pressures for the economy.[4]

Moreover, it is not only where goods are being produced that looks set to change, but also how. The war is likely to speed up the green transition as a means of reducing dependence on unfriendly actors. This could keep up pressure on the prices of fossil fuels as well as those of rare metals and minerals, although it could also cause some other prices to fall.

Indeed, green technologies are set to account for the lion’s share of the growth in demand for most metals and minerals in the foreseeable future. The faster and more urgent the shift to a greener economy becomes, the more expensive it may be in the short run.[5]

The combined effect of these shocks has been to raise inflation expectations from their pre-pandemic lows. Longer-term measures of market-based inflation compensation are now around 2.25%.[6] Survey-based measures of inflation expectations have also shifted upwards, with the median professional forecaster[7] and monetary analyst[8] now expecting 2% inflation over the longer term. And the inflation expectations of consumers have increased in parallel.[9]

The bulk of the distribution of different measures of inflation expectations are becoming centred around our target, rather than at much lower levels like before the pandemic. However, the “right tail” of the distribution is widening, which is a development we are monitoring closely.

All this suggests that, even when supply shocks fade, the disinflationary dynamics of the past decade are unlikely to return. As a result, it is appropriate for policy to return to more normal settings rather than those aimed at raising inflation from very low levels.

The uncertain growth outlook

We also have to take the growth outlook into account when calibrating policy normalisation.

A number of forces have been underpinning growth in the euro area, including the continued tailwinds from the reopening of the economy, the high stock of accumulated savings and the fiscal support introduced to offset higher energy bills. The labour market has also rebounded much faster than expected, with unemployment falling to a historic low.

However, the euro area is clearly not facing a typical situation of excess aggregate demand or economic overheating. Both consumption and investment remain below their pre-crisis levels, and even further below their pre-crisis trends. And the outlook is now being clouded by the negative supply shocks hitting the economy. This is evident from the fact that, in the near term, inflation and growth are moving in opposite directions.

In particular, a large share of the inflation we are experiencing today is imported from outside the euro area. This is acting as a terms of trade “tax”, which reduces the total income of the economy – even if we take into account the higher prices being earned by exporters. Cumulatively from the second quarter of 2021 to the first quarter of this year, the euro area transferred €170 billion, or 1.3% of its GDP, to the rest of the world.

Households are the ones suffering most from higher import prices, as rising energy and food inflation are eating into real incomes, and nominal wages are not yet catching up. In fact, real wage growth turned negative in the fourth quarter of last year – the last data point we have – and real wages are likely to be contracting even faster now due to rising inflationary pressures.

We do not yet have clear indications of how much consumption is being affected. But confidence indicators have reacted: households’ expectations of their future financial situation dropped to their second-lowest level on record in March and remained close to that level in April.

High energy costs and supply shortages are now also starting to be felt in industrial production, which contracted in nearly all major economies in March.

The path towards policy normalisation

So what should normalisation mean in this context?

With the inflation outlook having shifted notably upwards compared with the pre-pandemic period, it is appropriate for nominal variables to adjust – and that includes interest rates. This would not constitute a tightening of monetary policy; rather, leaving policy rates unchanged in this environment would constitute an easing of policy, which is not currently warranted.

Against the backdrop of the evidence I presented above, I expect net purchases under the APP to end very early in the third quarter. This would allow us a rate lift-off at our meeting in July, in line with our forward guidance. Based on the current outlook, we are likely to be in a position to exit negative interest rates by the end of the third quarter.

上記の証拠を背景に、APPの下での純購入は第3四半期の非常に早い時期に終了すると予想しています。 これにより、フォワードガイダンスに沿って、7月の会合で金利を引き上げることができます。 現在の見通しを踏まえると、第3四半期末までにマイナス金利を解消できる可能性があります。

The next stage of normalisation would need to be guided by the evolution of the medium-term inflation outlook. If we see inflation stabilising at 2% over the medium term, a progressive further normalisation of interest rates towards the neutral rate will be appropriate. But the pace and overall scale of the adjustment cannot be determined ex ante.

If the euro area economy were overheating as a result of a positive demand shock, it would make sense for policy rates to be raised sequentially above the neutral rate. This would ensure that demand falls back into line with supply and that inflationary pressures ease.

But the situation we are currently facing is complicated by the presence of negative supply shocks. This creates more uncertainty about the speed with which the current price pressures will abate, about the evolution of excess capacity, and about the extent to which inflation expectations will continue to remain anchored at our target.

In such a setting, there are arguments for gradualism, optionality and flexibility when adjusting monetary policy.[10]

Gradualism is a prudent strategy under uncertainty. In particular, since the neutral rate is unobservable and depends on many factors, we will only truly know where it is once we get there. This means that it is sensible to move step by step, observing the effects on the economy and the inflation outlook as rates rise.

Optionality is important to allow us to re-optimise the policy path as we go, especially as key variables underpinning that path will only become clearer with time.

The restrictive effect of supply shocks on growth means that demand is already, to some extent, being pulled back into line with supply. If these restrictive effects were to strengthen, the pace of normalisation would be slower.

At the same time, there are clearly conditions in which gradualism would not be appropriate. If we were to see higher inflation threatening to de-anchor inflation expectations, or signs of a more permanent loss of economic potential that limits resource availability, the optimal policy would become the same as for a demand shock: we would need to withdraw accommodation promptly to stamp out the risk of a self-fulfilling spiral.

Flexibility will help us to ensure the smooth and even transmission of our monetary policy across the euro area as normalisation proceeds.

For this reason, it is premature at this stage to discuss how the ECB’s balance sheet policies – in particular the reinvestment of the maturing stock of assets purchased under the PEPP and the APP – will interact with the process of interest rate normalisation. For the time being, our policy interest rates will act as the marginal tool for adjusting the policy stance.

Any future decisions on the balance sheet will have to be consistent with both the evolving medium-term inflation outlook and our pledge to ensure policy transmission – especially as flexible reinvestment of the PEPP portfolio is a tool we have made available to mitigate fragmentation risks.

If necessary, we can design and deploy new instruments to secure monetary policy transmission as we move along the path of policy normalisation, as we have shown on many occasions in the past.

Conclusion

To sum up, the environment facing monetary policy today has changed significantly from that which we confronted before the pandemic. The tools we were deploying at that time, aimed at combating persistent too-low inflation, are no longer appropriate.

But we are also not facing a straightforward situation of excess aggregate demand: in fact, supply shocks are raising inflation and slowing growth in the near term. This means that policy normalisation has to be carefully calibrated to the conditions we face.

The next step in rate normalisation will involve following through with our forward guidance on ending net asset purchases and on rate lift-off.

If we see inflation stabilising at 2% over the medium term, a progressive further normalisation of interest rates towards the neutral rate will be appropriate. But the speed of policy adjustment, and its end point, will depend on how the shocks develop and how the medium-term inflation outlook evolves as we move forward.

In the end, we have one important guidepost for our policy: to deliver 2% inflation over the medium term. And we will take whatever steps are needed to do so.

タカ派の不満

欧州中央銀行(ECB)のラガルド総裁はECBウェブサイトへのブログ投稿で、7-9月(第3四半期)末までにマイナス金利から脱却する可能性を示唆した。7月と9月の会合でいずれも0.25ポイントずつの利上げが行われることを示唆しており、事実上0.5ポイント利上げの選択肢を排除したことになる。より迅速なペースでの引き上げを選択肢として残しておきたい一部の当局者はそれに不満を抱いていると、複数の関係者が明らかにした。

Lagarde Says ECB Likely to Exit Negative Rates by End of September

- Net bond buying set to end ‘very early’ in third quarter

- Lagarde stresses that policy normalization will be gradual

By

Alexander Weber2022年5月23日 17:22 JSTUpdated on

Listen to this article

3:34

Share this article

Follow the authors@WeberAlexander+ Get alerts forAlexander Weberhttps://69f0693ec902492fe0c54cf964cd3dac.safeframe.googlesyndication.com/safeframe/1-0-38/html/container.html

In this article

EUREuro Spot1.0684EUR-0.0007-0.0655%

Sign up for the New Economy Daily newsletter, follow us @economics and subscribe to our podcast.

The European Central Bank is likely to start raising interest rates in July and exit sub-zero territory by the end of September, President Christine Lagarde said.

“I expect net purchases under the APP to end very early in the third quarter,” she said in a blog post Monday. “This would allow us a rate lift-off at our meeting in July, in line with our forward guidance. Based on the current outlook, we are likely to be in a position to exit negative interest rates by the end of the third quarter.”

With inflation running at almost four times the ECB’s 2% target, momentum in the central bank’s Governing Council has been building to raise the deposit rate from its current level of -0.5% in July. Lagarde’s comment suggests two increases of 25 basis points each at the July and September policy meetings.

While Dutch central bank chief Klaas Knot last week mentioned the possibility of a half-point rate hike if required, Lagarde has repeatedly said that policy normalization will be gradual, and reiterated that sentiment again on Monday.

“This means that it is sensible to move step by step, observing the effects on the economy and the inflation outlook as rates rise,” she said.

The euro advanced against the dollar after her comments, rising as much as 1% to 1.0674, the highest level in almost a month. 10-year German bonds erased earlier gains, with yields rising 4 basis points to 0.98%.

What Bloomberg Economics Says...

“Lagarde has taken the unusual step of essentially announcing in advance an interest rate increase in July and a second in September. This removes most of the doubt surrounding the ECB’s next moves and makes a 50 basis point hike in July unlikely.”

--David Powell, senior euro-area economist. For full Insight, click here

Russia’s invasion of Ukraine has sent commodity prices higher while increasing uncertainty about the outlook and denting confidence among businesses and households. That’s created a difficult situation for policy makers as any measures to contain inflation also threaten to slow activity further.

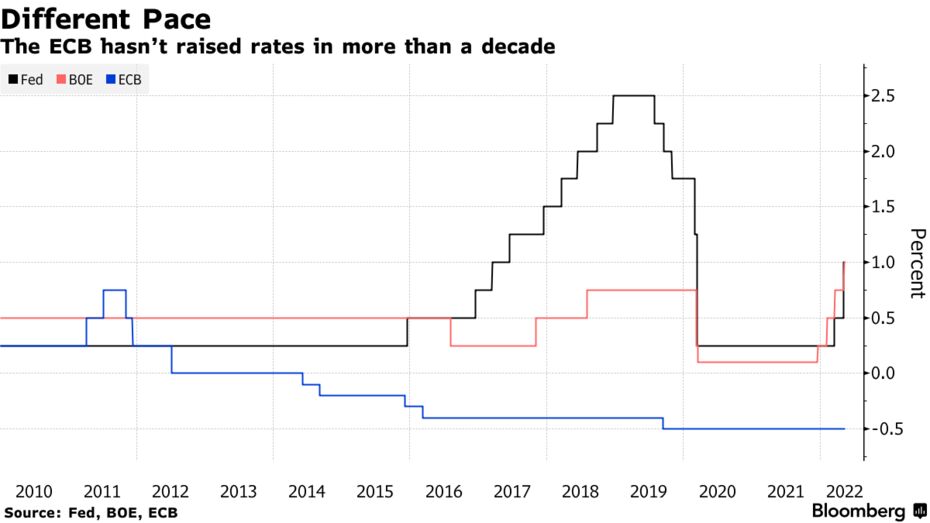

Raising the deposit rate by 50 basis points through September would still put the central bank behind peers like the Federal Reserve and the Bank of England, who’ve increased borrowing costs this year to quell surging inflation.

Weak Euro

That’s also helped weaken the euro in recent months, compounding the challenge for ECB officials because that makes imports -- a key source of current inflation -- more expensive.

Lagarde, who said she wanted to “clarify the path of policy normalization that lies ahead of us” with her blog post, noted the ECB needs to keep its options open because of uncertainty about future price growth.

“Optionality is important to allow us to re-optimize the policy path as we go, especially as key variables underpinning that path will only become clearer with time,” Lagarde said. That could also mean withdrawing monetary stimulus “promptly to stamp out the risk of a self-fulfilling spiral.”

The prospect of the first rate hike in more than a decade has increased concern about a potential bond-market fragmentation among the 19 members of the currency bloc, as governments increased their debt loads to help the economy deal with the Covid-19 pandemic. Sponsored ContentHow Sun, Wind and Water Will Power Angola's EconomyAipex

Lagarde reiterated that the ECB would also be able to “design and deploy new instruments” to make sure that monetary policy is properly transmitted through the euro area.

— With assistance by Libby Cherry(Updates with Bloomberg Economics in seventh paragraph)

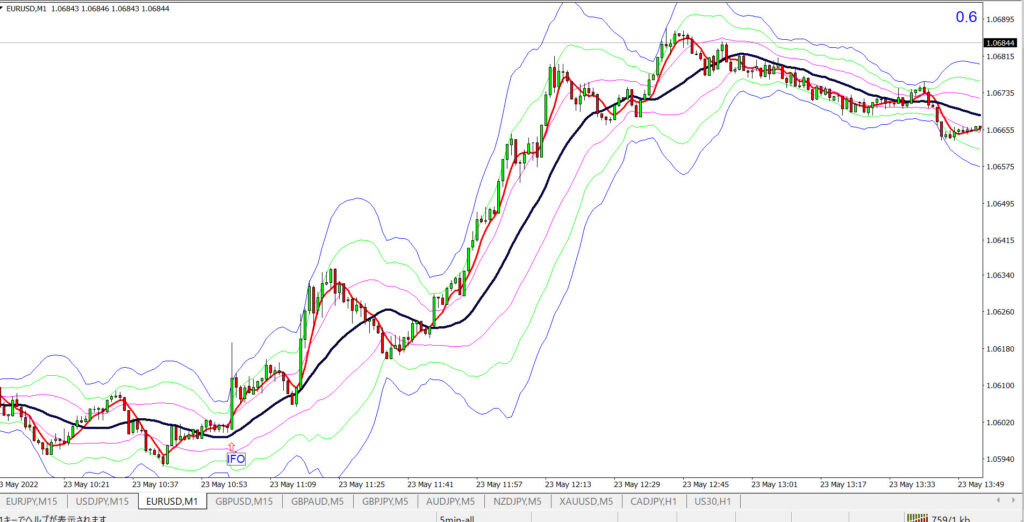

5分足↓

1分足↓ IFOは17:00 予想 91.4 結果93.0 と良かったため、上がったのだろう。更にラガルド発言があって上がった(これは間違いない)。